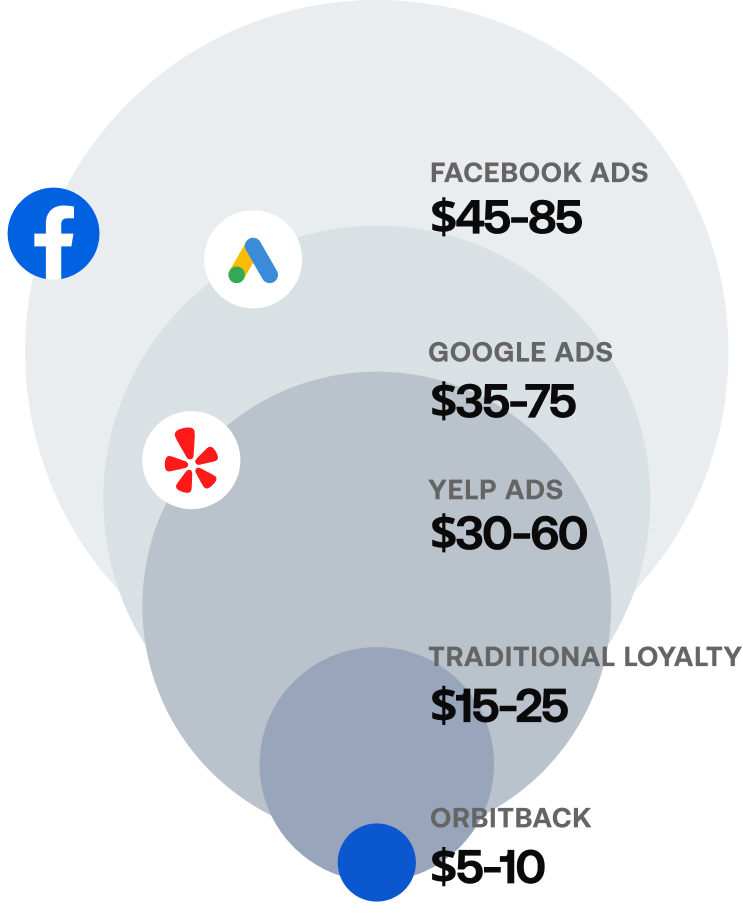

The short answer

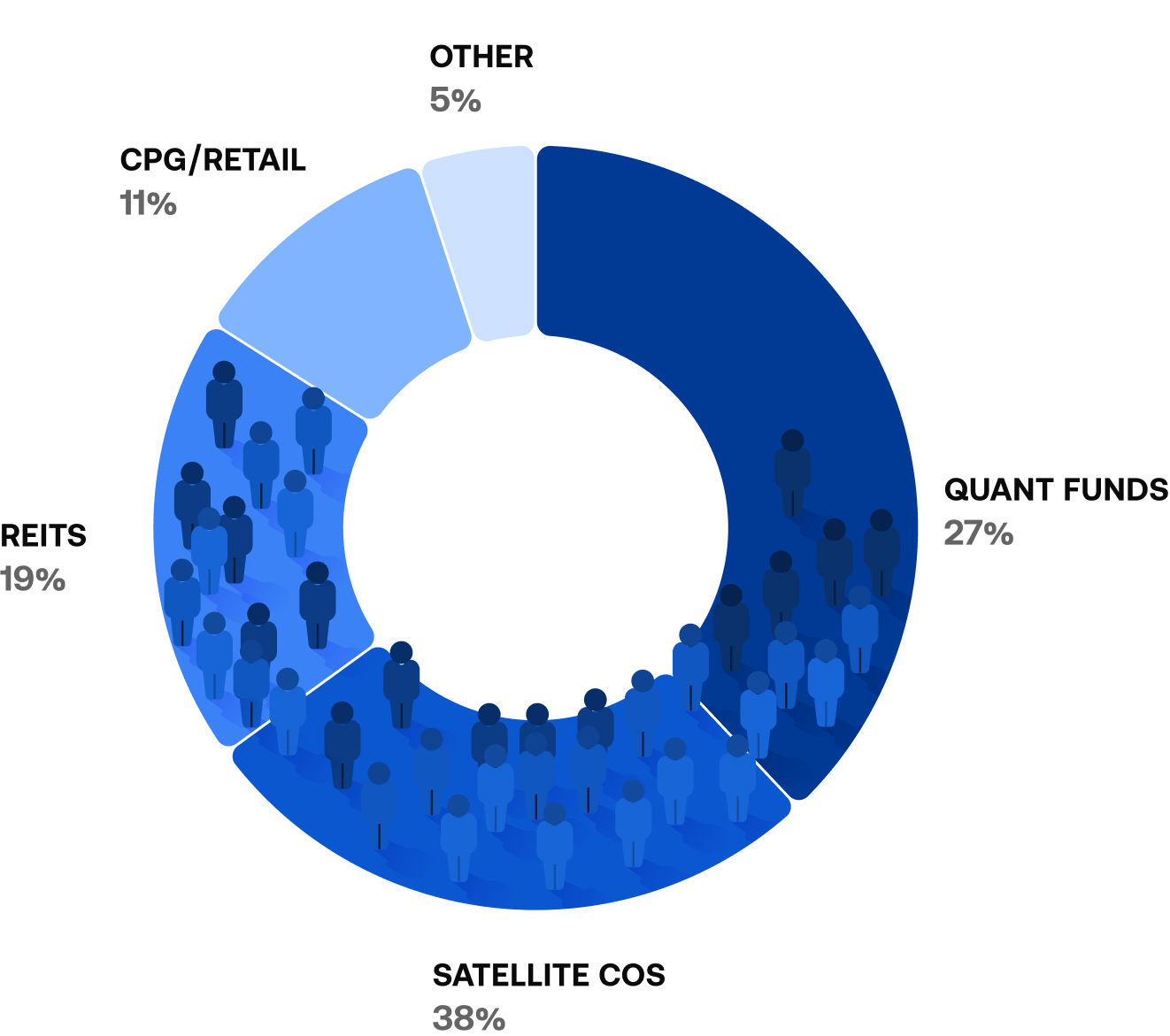

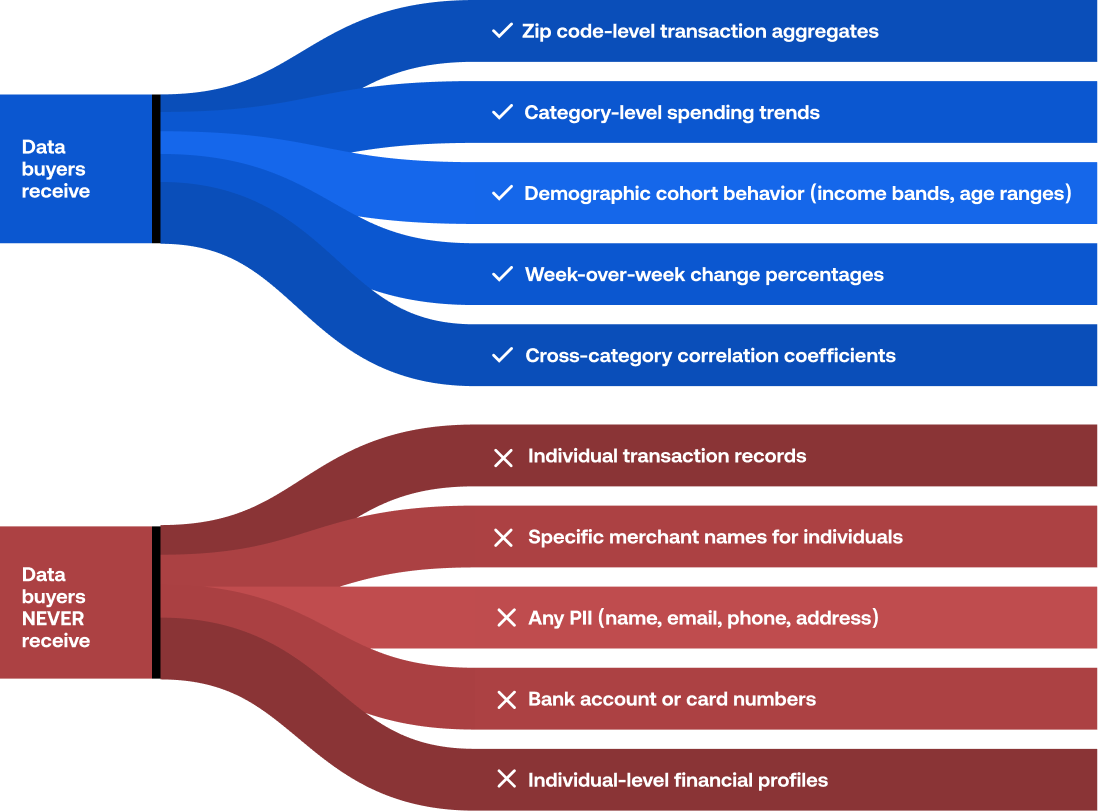

We collect subscription fees from your customers ($10-$40/month depending on tier). We also sell anonymized, aggregated spending pattern data to institutional research buyers—satellite imagery companies, quantitative hedge funds, real estate investment trusts, and urban planning firms.

Your customers' personal information is never sold.No. And we mean that — this platform was built specifically because we were sick of services that prey on small businesses with fees buried in the fine print. No email fees. No hosting fees. No "premium support" fees. No per-transaction processing fees. No monthly minimums. No setup fees. No cancellation fees. No annual renewal fees. No feature unlock fees.

That's it. But to understand why anyone would pay for that—and pay well—you need to understand a $7.2 billion industry hiding in plain sight.

$7.2BAlternative data market (2024)

$7.2BAlternative data market (2024) 29.3%CAGR through 2030

29.3%CAGR through 2030'%20fill='%233186FF'/%3e%3cpath%20d='M81.7324%2031.1277L33.4235%203.23514L33.4249%2048.5017L81.7338%2074.1854L81.7324%2031.1277Z'%20fill='%230B57D0'/%3e%3cpath%20d='M81.7325%2023.0646C81.7325%2021.98%2080.9651%2020.6612%2080.0259%2020.1316L68.8962%2013.8553C67.3564%2012.987%2066.1176%2013.7184%2066.1176%2015.4965C66.1176%2016.9671%2066.1176%2018.6232%2066.1176%2019.7206C66.1176%2022.1113%2063.7962%2023.9283%2059.0492%2021.0939C49.693%2015.5074%2081.7328%2033.7438%2081.7328%2033.7438L81.7325%2023.0646Z'%20fill='%230B57D0'/%3e%3crect%20width='54.5544'%20height='47.6232'%20transform='matrix(-0.866014%20-0.500019%203.18914e-05%201%2078.7676%2031.8152)'%20fill='white'/%3e%3crect%20width='54.5544'%20height='47.6232'%20transform='matrix(-0.866014%20-0.500019%203.18914e-05%201%2076.3262%2033.6393)'%20fill='%23ECECEC'/%3e%3crect%20width='54.5544'%20height='47.6232'%20transform='matrix(-0.866014%20-0.500019%203.18914e-05%201%2073.6836%2035.2657)'%20fill='white'/%3e%3cpath%20d='M70.4864%2040.426C70.4864%2038.8775%2069.3993%2036.9946%2068.0583%2036.2203L25.4148%2011.5989C23.6268%2010.5665%2022.1775%2011.4034%2022.1775%2013.4679L22.1788%2052.1925C22.1788%2053.7409%2023.2659%2055.6238%2024.6069%2056.3981L70.4878%2082.8888L70.4864%2040.426Z'%20fill='%23549AFF'/%3e%3cpath%20d='M42.5242%2064.0437L27.1742%2055.1937L11.8242%2064.0437C20.2992%2068.9187%2034.0492%2068.9187%2042.5242%2064.0437Z'%20fill='%233186FF'/%3e%3cpath%20d='M42.5242%2079.5937V55.2437L11.8242%2054.8937V79.5937C20.2992%2084.4937%2034.0492%2084.4937%2042.5242%2079.5937Z'%20fill='%237CA411'/%3e%3cpath%20d='M42.5242%2064.0437L27.1742%2055.1937L11.8242%2064.0437C20.2992%2068.9187%2034.0492%2068.9187%2042.5242%2064.0437Z'%20fill='%239DC82A'/%3e%3cpath%20d='M11.8242%2064.0437L27.1742%2055.1937L6.44922%2058.9187C7.44922%2060.7687%209.24922%2062.5437%2011.8242%2064.0437Z'%20fill='%233186FF'/%3e%3cpath%20d='M27.1733%2055.1687L42.5232%2064.0187C50.9982%2059.1187%2050.9982%2051.1937%2042.5232%2046.2937C34.0482%2041.3937%2020.2982%2041.3937%2011.8232%2046.2937C5.92324%2049.6937%204.12325%2054.5937%206.44824%2058.8937L27.1733%2055.1687Z'%20fill='%23AFD0FF'/%3e%3cpath%20d='M42.5234%2079.5937C46.7984%2077.1437%2048.8985%2073.8937%2048.8735%2070.6687V55.3187C48.7985%2058.4687%2046.6984%2061.6187%2042.5234%2064.0187V79.5937Z'%20fill='%23959595'/%3e%3cpath%20d='M5.47266%2071.0687C5.52266%2072.2187%205.84766%2073.3687%206.44766%2074.4687V58.8937C5.84766%2057.7937%205.52266%2056.6437%205.47266%2055.4937V71.0687Z'%20fill='%2391BEFF'/%3e%3cpath%20d='M6.44922%2074.4687C7.44922%2076.3437%209.24922%2078.1187%2011.8242%2079.5937V64.0187C9.24922%2062.5437%207.44922%2060.7687%206.44922%2058.8937V74.4687Z'%20fill='%230B57D0'/%3e%3c/svg%3e) 78%Hedge funds using alt data

78%Hedge funds using alt data $1.1MAvg. annual spend per fund

$1.1MAvg. annual spend per fund

ε = 0.1

ε = 0.1'%3e%3cpath%20d='M26.5176%2028.219L26.5176%2070.9805L26.5176%2072.1602L77.9784%2072.1602L77.9784%2028.219L26.5176%2028.219Z'%20fill='%23AFD0FF'/%3e%3ccircle%20cx='21.0762'%20cy='21.0762'%20r='21.0762'%20transform='matrix(-0.866025%200.5%20-0.866057%20-0.499945%2088.6328%2071.0521)'%20fill='%23AFD0FF'/%3e%3ccircle%20cx='22.702'%20cy='22.702'%20r='22.702'%20transform='matrix(-0.866025%200.5%20-0.866057%20-0.499945%2091.4453%2026.8851)'%20fill='%23488DEF'/%3e%3cpath%20d='M24.3266%2020.3955L24.304%2027.88L29.0525%2025.3323L24.3266%2020.3955Z'%20fill='%23488DEF'/%3e%3cpath%20d='M79.8956%2021.3542L79.8843%2026.5452L75.6709%2021.6334L79.8956%2021.3542Z'%20fill='%23488DEF'/%3e%3ccircle%20cx='22.702'%20cy='22.702'%20r='22.702'%20transform='matrix(-0.866025%200.5%20-0.866057%20-0.499945%2091.4453%2021.1238)'%20fill='%2367A6FF'/%3e%3crect%20x='49.6777'%20y='47.9959'%20width='5.14057'%20height='33.7056'%20rx='1.66982'%20fill='%2391BEFF'/%3e%3crect%20width='5.14057'%20height='33.7056'%20rx='1.66982'%20transform='matrix(0.956305%200.292372%200%201%2039.502%2045.4096)'%20fill='%2391BEFF'/%3e%3crect%20width='5.14057'%20height='33.7056'%20rx='1.66982'%20transform='matrix(0.819152%200.573576%200%201%2030.2617%2040.8779)'%20fill='%2391BEFF'/%3e%3crect%20width='5.14057'%20height='33.7056'%20rx='1.66982'%20transform='matrix(0.857167%20-0.515038%200%201%2069.1504%2043.8262)'%20fill='%2391BEFF'/%3e%3crect%20width='5.14057'%20height='33.7056'%20rx='1.66982'%20transform='matrix(0.97437%20-0.224951%200%201%2059.7754%2047.1512)'%20fill='%2391BEFF'/%3e%3crect%20width='4.17415'%20height='4.17415'%20transform='matrix(0.86601%200.500028%203.18351e-05%201%2055.4023%2014.2576)'%20fill='white'/%3e%3crect%20width='4.17415'%20height='4.17415'%20transform='matrix(0.86601%20-0.500028%20-3.18351e-05%201%2051.7871%2016.3432)'%20fill='white'/%3e%3crect%20width='4.17415'%20height='4.17415'%20transform='matrix(0.866041%200.499972%20-0.866041%200.499972%2055.4023%2018.4305)'%20fill='%233186FF'/%3e%3crect%20width='10.0307'%20height='4.17415'%20transform='matrix(0.86601%200.500028%203.18351e-05%201%2046.7168%2013.4145)'%20fill='%233B8CFF'/%3e%3crect%20width='4.17415'%20height='4.17415'%20transform='matrix(0.86601%20-0.500028%20-3.18351e-05%201%2055.4023%2018.4305)'%20fill='%232563EB'/%3e%3crect%20width='4.17415'%20height='9.93307'%20transform='matrix(0.866041%20-0.499972%200.866041%200.499972%2046.7949%2013.4634)'%20fill='white'/%3e%3ccircle%20cx='18.9328'%20cy='18.9328'%20r='18.9328'%20transform='matrix(0.86601%200.500028%203.18489e-05%201%2011.625%2033.4177)'%20fill='%23688F00'/%3e%3cpath%20d='M31.8403%2086.3771L40.0798%2081.6421L36.2598%2079.2748L31.8403%2086.3771Z'%20fill='%23688F00'/%3e%3cpath%20d='M9.03711%2046.0308L15.941%2042.0558L14.1502%2047.1469L9.03711%2046.0308Z'%20fill='%23688F00'/%3e%3ccircle%20cx='18.9328'%20cy='18.9328'%20r='18.9328'%20transform='matrix(0.86601%200.500028%203.18489e-05%201%203.83203%2037.9177)'%20fill='%23BAE449'/%3e%3cpath%20d='M16.2963%2051.9095C16.5873%2051.9877%2016.9189%2052.1874%2017.1833%2052.5205C17.336%2052.7122%2017.4261%2052.9495%2017.4784%2053.169C18.4659%2056.9466%2019.4759%2060.7277%2020.4542%2064.503C20.7652%2064.6914%2021.0814%2064.8935%2021.3735%2065.2006C21.9617%2065.7994%2022.4311%2066.6591%2022.6023%2067.4579C22.7755%2068.2354%2022.6664%2068.9356%2022.3123%2069.3069C21.9895%2069.6589%2021.4638%2069.7234%2020.9012%2069.4802C20.3642%2069.2536%2019.8011%2068.7521%2019.3758%2068.1184C18.9105%2067.4362%2018.6138%2066.6099%2018.5897%2065.9179C18.563%2065.3564%2018.7121%2064.8928%2018.9934%2064.6162C17.9552%2060.6608%2016.9108%2056.7042%2015.8715%2052.7488C15.7368%2052.258%2015.9263%2051.8379%2016.2963%2051.9095Z'%20fill='%230B57D0'/%3e%3cpath%20d='M28.5937%2066.6892C28.9831%2066.8537%2029.4038%2067.1273%2029.741%2067.5776C30.4025%2068.3779%2030.7181%2069.5518%2030.4717%2070.2278C30.3052%2070.7298%2029.8615%2070.9434%2029.3399%2070.809C28.5938%2070.6333%2027.8601%2070.509%2027.1125%2070.3271C26.6247%2070.2389%2026.1328%2070.1347%2025.6373%2070.0155C25.1357%2069.9252%2024.6284%2069.814%2024.1196%2069.6947C23.5221%2069.5829%2022.9201%2069.4536%2022.3139%2069.3048C22.668%2068.9335%2022.7771%2068.2333%2022.6039%2067.4558C22.4327%2066.657%2021.9633%2065.7973%2021.3751%2065.1985C21.4412%2065.1799%2021.516%2065.184%2021.5954%2065.205C23.4836%2065.5917%2025.3779%2066.0063%2027.2671%2066.3971C27.7154%2066.5199%2028.1438%2066.5572%2028.5937%2066.6892Z'%20fill='white'/%3e%3c/g%3e%3cdefs%3e%3cclipPath%20id='clip0_676_257'%3e%3crect%20width='90'%20height='90'%20fill='white'/%3e%3c/clipPath%3e%3c/defs%3e%3c/svg%3e) 72hrs

72hrs 30K+

30K+ 0

0